Oracle is not the only software company accused of using predatory audit tactics to drive sales of its software products. In 2013 an

The facts alleged in the Complaint about

Each day we see cases where software companies vastly inflate audit findings in a transparent attempt to obtain leverage over their customers, and force a large software purchase. There are strategies that can be employed before and during the audit to mitigate the risk of such excessive findings. Unfortunately many companies are "penny wise and pound foolish" and don't seek professional help before or during the audit, but instead wait till the issuance of the final audit report. This is a mistake.

Enterprise software customers really need to be proactive in managing their licenses well before the audit notice arrives. And do not let software companies use the audit as a tool to force your company to give up older and perhaps more favorable licenses. In our experience, enterprise software companies sometimes use audits to try to push their customers to migrate from older, more favorable licenses to ones that are better for the licensor. Companies buy perpetual licenses for a reason and should be skeptical of software vendors using inflated audit findings to force a customer to give up valuable contractual rights.

If a software company tells you that they are going to conduct a friendly audit to right size your IT footprint and to optimize your licenses, this should be an immediate red flag. Enterprise software companies are not out to help you, but only to sell more software. Plaintiff here alleges that

Sometimes software vendors will hire third parties to conduct the audit. And that is what apparently happened here, with

Before the audit is commenced, the licensee should hammer out the scope of the audit and set some ground rules. Be proactive, take control and most importantly, stand strong. Software vendors do not like squeaky wheels, and prefer easy targets. The more you push back and the harder you make it for the software company, the less likely the software vendor will be to target you in the future.

The Cimino Complaint alleges that the initial audit results found very little in terms of non-compliance. Plaintiff then alleges that

We also have observed software companies employing similar tactics during audits. In fact, it is our opinion that this is why Oracle usually comes up with a huge shock number in its Final Audit Report. Oracle does not quantify the shock number in the Final Report but just identifies the number of licenses Oracle claims the customer is under licensed. Oracle leaves it to the licensee to "do the math". In our opinion, this is all part of the Oracle playbook to create leverage for the follow-up by the Oracle Sales Team, which works hand in hand with the Oracle auditors.

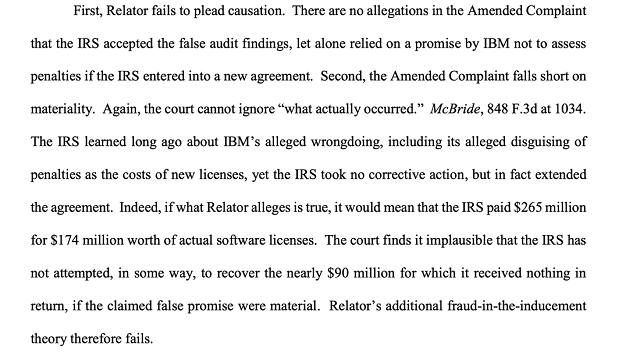

The Complaint alleges that in order to avoid paying these penalties, the

Cimino asserts that the

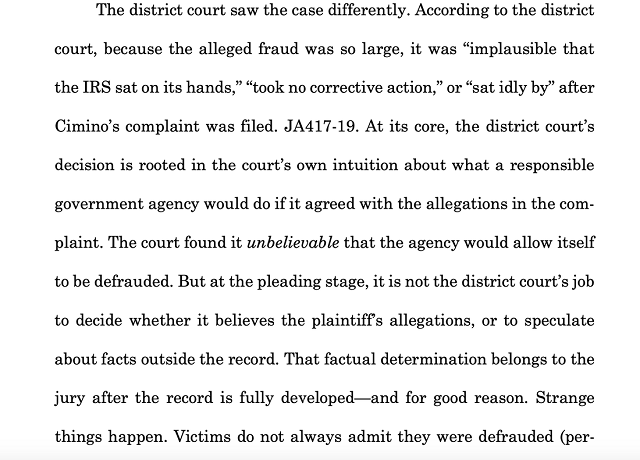

But in dismissing Cimino's Complaint, the Judge did not find it credible that the

According to the Court, Relator (Cimino) failed to plead causation and to show that the fraudulent audit findings was what induced the

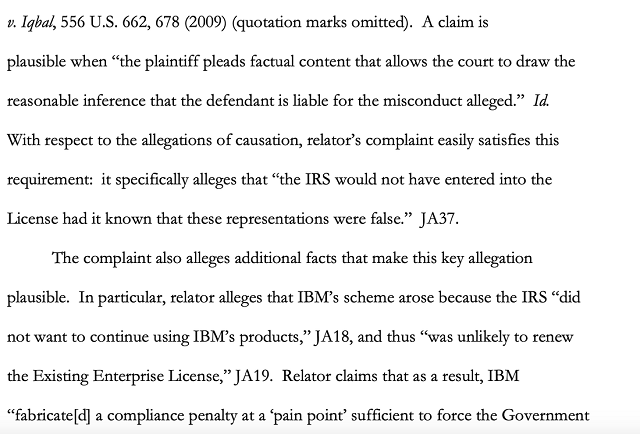

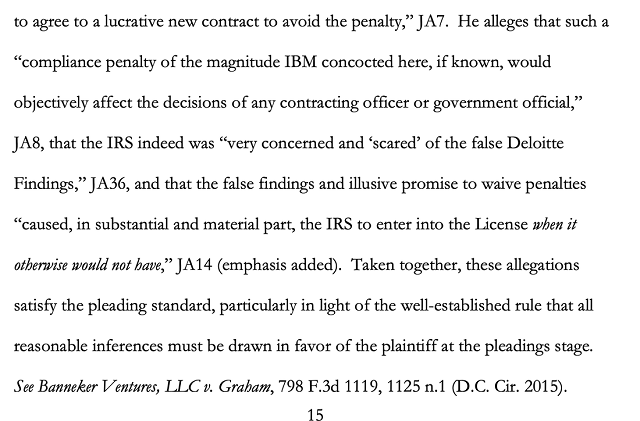

Well Judge, you may not believe it, but I do. I think that the Court is wrong here. The Complaint pleads that it was the fraudulent audit findings and the desire to get out from under the audit findings and related penalties that drove the

In my view, this extremely important whistleblower suit should never have been dismissed at the pleading stage. Cimino should be given the opportunity to take discovery and go forward with his case. Cimino's brief says it best here:

Victims do not always admit they have been defrauded. That rings so true. Give

Whether you are a Fortune 500 company or a municipality or governmental entity, you can be a victim of predatory audit practices by aggressive software vendors. We help companies and governmental agencies to fight back against such tactics.

The case is

Originally published

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

Ms

Four Embarcadero Center, Suite 1400

CA 94111

Tel: 415766 3509

Fax: 415231 5272

E-mail: pam@tacticallawgroup.com

URL: www.tacticallawgroup.com

© Mondaq Ltd, 2020 - Tel. +44 (0)20 8544 8300 - http://www.mondaq.com, source