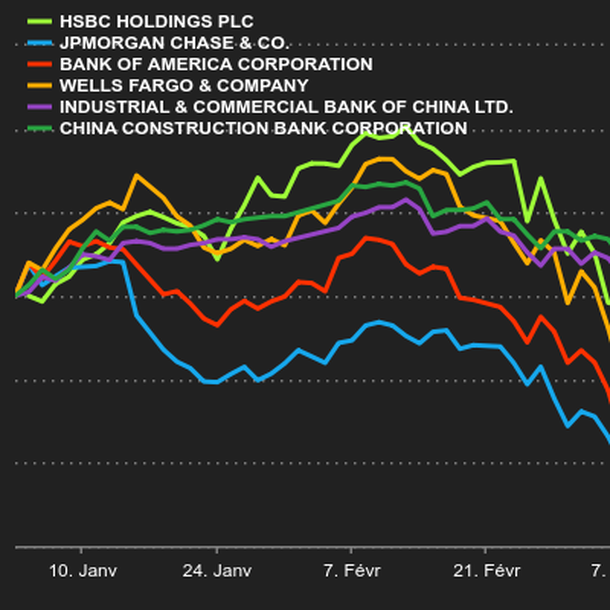

|

Monday November 18 | Weekly market update |

| Uncertainties about trade negotiations have somewhat dampened operators' enthusiasm last week, despite some optimism about the imminent signing of a Phase 1 agreement. However, this enthusiasm did not benefit all geographical areas, as Asia remained impacted by the violent demonstrations in Hong Kong while the United States set historical records. |

| Indexes Over the past week, Asian indices have lost ground against the current of other financial markets. The Nikkei lost 0.38%. The Hang Seng fell by 4.7% with the resurgence of tensions in Hong Kong and the return to recession, a first in 10 years (see graph). The Shanghai Composite declined by 2.4%. In Europe, at the time of writing, the CAC40 is once again performing well, with a gain of 0.6%. The Dax is down by 0.2% and Footsie by 1%. As for the peripheral countries of the euro zone, Portugal lost 0.8% over the week and Spain lost 2%. In the United States, performances are positive. The Dow Jones rose 0.7%, the S&P500 and the Nasdaq100 gained 0.5%. Evolution of the Hang Seng and Hong Kong growth  |

| Commodities After OPEC's bleak picture of the outlook for oil markets, it is now the International Energy Agency's (IEA) turn to publish its forecasts. The institution sees a paradoxically stable market since the abundant supply should compensate for the multiplication of geopolitical tensions. Oil prices thus stabilized this week despite the further increase in US inventories. Brent is still trading around USD 61.5 while WTI is trading at USD 56.5. Gold and silver timidly regain some colours after the heavy releases of the previous week. Risk appetite remains as strong as ever, as evidenced by the growth in equity markets. The gold metal earns a few dollars at USD 1465, the silver on its side consolidates at USD 16.87. The industrial metals segment fell sharply over the week, weighed down by the rise of the US dollar and the lack of progress on the commercial front. Copper lost ground at USD 58735, as did aluminum and tin at USD 1756 and 16185 respectively. |

| Equities markets Jumbo Interactive: the Australian FDJ! Jumbo is one of the leading digital retailers of national and charity lotteries through a range of digital platforms. The 2019 financial year, which has just ended, shows that performance is on track, with a strong increase in revenues and profits. The company divides its business into platforms for digital gaming and a SaaS service to provide software to other lottery operators. The $26 million in net income rewards shareholders, with a total of 37 cents per share, a return close to 2%. The stock has risen 187% since the beginning of the year, ranking as the third best performer in the Sydney Major Index (ASX200), accumulating more than 3800% in total over ten years. The Brisbane company is approaching $1 billion in capitalization. Jumbo stock chart  |

| Bond market Since mid-August, government bond yields have gradually rebounded. The yield on 10-year US bonds almost reached 2% again and fell to 1.83%. The yield of the German Bund went from -0.7% to -0.35% in three months. The French OAT also sees its rate duplicate these trajectories, thus returning close to zero. Italian and Spanish debts generate 1.30% and 0.44% respectively. Even the Swiss Confederation's bonds went from a yield of -1.2% to -0.55%. Does this suggest an exit from negative rates and a return to inflation? It seems difficult, to date, to imagine an extension of this rate hike, with the global debt stock estimated at $250 trillion, or 240% of global GDP. This is an incentive for central banks to stay on track with accommodative strategies. |

| Forex market The British pound benefited from the announcement of GDP growth in the United Kingdom. Gross domestic product grew by 0.3% in the third quarter, after a decline of 0.2% in the second quarter. Two consecutive quarters of declining GDP are considered a technical recession. The cable was GBP 1.29, an increase of 130 basis points and GBP 0.855 against the euro. Nevertheless, the single currency stabilised its decline after the publication of the German growth (0.1%), a statistic that raised the EUR/USD parity to 1,102 USD. Despite a euphoric equity climate, the yen, traditionally a safe haven, remains sought by traders, performing a bullish move against the greenback, at 108.50 for the USD/JPY parity instead of 109.30. Industrial production in Japan rebounded by 1.7% in September and is no stranger to the valuation of the Japanese currency. |

| Economic data Germany avoids recession in the third quarter. The country recorded a slight rebound of 0.1% in its gross domestic product, after a decline of 0.2% in the previous three months. Two consecutive quarters of contraction would have effectively weighed on the euro zone. Consumption has kept a positive figure. On the other hand, equipment investment declined, reflecting the sluggishness of the manufacturing sector, which is still in recession. The economic situation should intensify the debate on the need for fiscal stimulus measures. Investors are therefore making an appointment at the end of next week to find out how SMIs are developing in Europe, with the Flash publications of services and especially industry on the euro zone, indicators established by the Markit Institute, the latest publication of which was 45.7 (see graph). Euro zone flash manufacturing PMI  |

| Good start for the last stock market month November" options and futures contracts have just once again offset the rise in the CAC40 and the original situation, the last stock market month in 2019 therefore begins at historical levels. Strong reduction in political stress, economic growth that has probably reached a low point and the stabilisation of the accommodative monetary environment are the drivers of the rise in equities. Risk On" arbitrage intensified, confirmed by a significant increase in sovereign bond yields. However, this stock market euphoria does not corroborate with new lower levels on the Vix. |