DeFi Technologies : As DeFi gathers momentum, how will regulators protect investors?

August 25, 2021 at 06:40 am EDT

Share

Decentralised (DeFi) Exchanges continue to gain a growing number of users as the level of trading and wide selection of assets and services they offer expands.

The total value of assets in DeFi is now over $84billion compared to only $1.8 billion in June 2021. So, what is driving this expansion of DeFi?

DeFi enables owners of cryptocurrencies to earn interest and allows one to borrow, lend and buy insurance, or just speculatively trade.

In effect, DeFi aims to offer owners of cryptocurrencies a range of services in a decentralised manner – typically offered by traditional financial markets which rely on centralised exchanges and clearing houses.

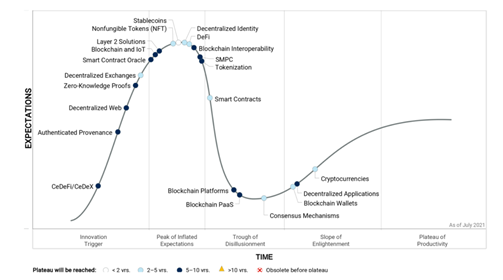

Hype cycle for Blockchain – July 2021:

Source: Gartner.com

Gartner believes that DeFi has two to five years before it reaches a plateau of productivity – i.e., when the technology starts to enjoy mainstream adoption which, in reality, is not very long for a technology that could shake the foundations of the financial services sector.

Using smart contracts, DeFi is looking ‘strip out’ much of the friction costs that accumulate due to the necessity of dealing with multiple intermediaries together with the need for audits and checks, regulatory compliance monitoring, and associated fees and costs – all of which stifle many existing traditional financial services today. Interestingly, Harvard Business Review cites a comparison between Yield Farming versus Foreign Currency Carry Trading:

“The search for passive returns on crypto assets – “yield farming” – is already taking shape on a number of new lending platforms. Compound Labs has launched one of the biggest DeFi lending platforms, where users can now borrow and lend any cryptocurrency on a short-term basis at algorithmically determined rates.

“A prototypical yield farmer moves assets around pools on Compound, constantly chasing the pool offering the highest annual percentage yield (APY). Practically, it echoes a strategy in traditional finance – a foreign currency carry trade – where a trader seeks to borrow the currency charging a lower interest rate and lend the one offering a higher return.

“Crypto yield farming, however, offers more incentives. For instance, by depositing stablecoins into a digital account, investors would be rewarded in at least two ways. First, they receive the APY on their deposits. Second, and more importantly, certain protocols offer an additional subsidy, in the form of a new token, on top of the yield that it charges the borrower and pays to the lender”.

Interest in using DeFi lending has increased as more people access pools of borrowing facilities, whether they be holders of Digital Assets looking to generate a yield on the Digital Assets they own or borrowers wishing to increase their exposure to this asset class.

Forbes has described DeFi lending as: “Unlike with a traditional bank, borrowers using DeFi apps cannot be held accountable with physical assets if unable to effectively pay back a loan. DeFi applications are similar to smartphone applications, but they built with smart contracts”.

CoinmarketCap, which tracks cryptocurrency prices in real-time, lists a variety of other lenders and DeFis apps where yield farming returns vary from 0.2% p.a to over 40%.

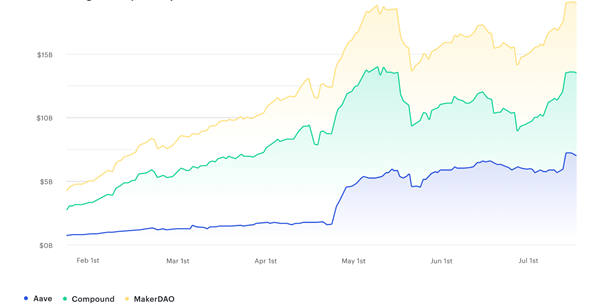

The three largest DeFi app lenders – Aave, Compound and MakerDao:

Source: Dune Analytics @hagaetc

In turn, Harvard Business Review has proposed that: “DeFi offers a less volatile and more accessible point of entry than other markets – and may just have enough appeal to bring blockchain into the mainstream.”

Should this prophetic statement be shown to be true, it is easy to understand, therefore, why DeFi could prove to be so attractive – not just for borrows and lenders, but so very disruptive for other sectors in the financial services industry.

A combination of greater transparency, afforded by using blockchain technology, and using smart contracts to eliminate human error ought to lead to more robust systems and procedures that regulators, investors and service providers can benefit from.

The losers potentially will be the intermediaries, auditors, lawyers and compliance consulting firms which are currently so prevalent in the financial services sector. It is indeed a powerful and alluring prospect that DeFi offers the potential for lower transaction costs, greater transparency (so enhanced trust) and a more robust compliance infrastructure.

If this proves to be the case and DeFi is indeed able to handle large volumes of transactions, then traditional financial services firms are likely to adopt this lower risk and alternative way of doing business, or be forced to do so by regulators.

One of the challenges that DeFi faces is that currently many of the DeFi services are built on the Ethereum blockchain and the price of transactions (gas fees) can mean that the costs outweigh the benefits.

Ethereum is attempting to address the gas fees but for now DeFi is very reliant on Ethereum – so expect to see other DeFi platforms being created using other Blockchains.

Mathew McDermott, head of Digital Assets at Goldman Sachs, recently stated: “In the next five to 10 years, you could see a financial system where all assets and liabilities are native to a blockchain, with all transactions natively happening on chain. So, what you’re doing today in the physical world, you just do digitally, creating huge efficiencies.

“And that can be debt issuances, securitization, loan origination; essentially, you’ll have a digital financial markets ecosystem, the options are pretty vast.”

However, surely for mainstream adoption regulators will search for some degree of accountability in the event of hacks or a DeFi app not delivering what has been promised.

One possible solution is could we see regulators turning to the Blockchain providers, such as Ethereum, and have them essentially act as gate keepers to vet the organisations that use their Blockchains and build DeFi apps.

Could we see Ethereum and other blockchains establishing some type of investor compensation scheme and then, DeFi platforms that run on their blockchains being granted regulatory approval?

Alternatively, will we see some traditional exchanges such as NASADAQ or the London Stock Exchange offer DeFi platforms, so regulators have a known entity to hold accountable?

Dr Jane Thomason from Novum Insights (a firm that specialises in analysing DeFi assets) when asked for her thoughts said: “”DeFi investors can lose money because activities are not regulated, moderated, intermediated, hosted or validated by a central authority, only driven by smart contracts.

“If the smart contract malfunctions, is hacked, or otherwise has a problem, there is no recourse. Who and what gets regulated? Its a global 24/7, borderless market. Regulators need to get their thinking caps on and learn to audit code! This is a whole new ball game.”

The balance between totally decentralised systems and procedures where it may be difficult to hold an entity accountable in a particular jurisdiction (and so be able to recompense and protect investors) will need to be addressed.

Increasingly, as our societies and lifestyles become more on-line and digital it is likely to present greater logistical challenges for regulators and governments to afford investor protection.

What will not alter and may potentially be even more relevant surely is:

“Caveat emptor”

Let the buyer beware.

The post As DeFi gathers momentum, how will regulators protect investors? appeared first on CityAM.

DeFi Technologies Inc. is a Canada-based crypto native technology company. The Company identifies opportunities and builds and invests in new technologies and ventures to provide diversified exposure across the decentralized finance ecosystem. The Company's subsidiary, Valour Inc., is an issuer of exchange traded products (ETPs) that provide simplified access to digital assets, has launched three euro-denominated products on NGM - Valour Ethereum Zero EUR, Valour Solana EUR, and Valour Digital Asset Basket 10 (VDAB10) EUR. Valour Ethereum Zero EUR tracks the price of ETH without charging management fees. Valour Solana EUR tracks the price of SOL, the native cryptocurrency fuelling the Solana network. Solana has more than 400 live projects spanning its DeFi, NFT, and Web3 ecosystem. Valour Digital Asset Basket 10 (VDAB10) tracks the performance of the 10 largest crypto assets based on market capitalisation with a maximum cap of 30% for any constituent.