Few think another G7 central bank would be bold enough to intervene directly as Japan did on Thursday. But they say markets should prepare for more verbal intervention and more aggressive rate hikes as policymakers try to thwart the U.S. currency's ascent.

The dollar is up 16% this year against a basket of other major currencies, on track for its biggest annual jump since at least the 1970s.

"There is an incentive for central banks to move faster. They realise it is better to frontload rate hikes and try and avoid further currency depreciation," said Ugo Lancioni, head of global currency at fund manager Neuberger Berman. Lancioni, who holds a long dollar position, added some in Europe want a stronger currency, which means this BOJ move is not unwelcome.

The G7 group of rich countries, which includes the United States and Japan, has a longstanding agreement that markets decide currency rates. But Japanese policymakers have said it gives Tokyo leeway to counter sharp moves.

Japan's Finance Minister Shunichi Suzuki said Japan had good communication with the United States, but declined to say whether Washington had consented to Tokyo's first intervention to support then yen since 1998.

The dollar surge follows aggressive Federal Reserve interest rate hikes, recession fears and geopolitical uncertainty following Russia's invasion of Ukraine.

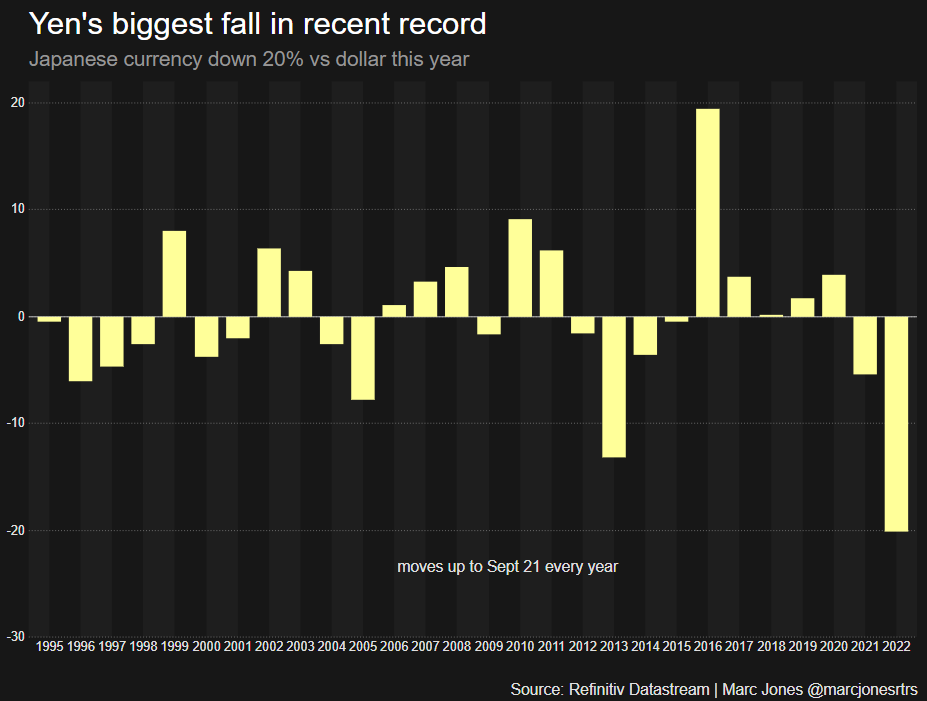

The scale and the speed of dollar gains - the latter arguably more important for policymakers - have been eye-watering. The yen, its central bank sticking to ultra-loose policy even as others raise rates, has been the biggest loser.

The dollar is up 23% versus the yen this year, its biggest move in at least 27 years, and nearly 10% since early August.

Graphic: Yen sees historic drop

Against the Swedish crown the dollar is up 22%; sterling has lost 17% to hit 37-year lows and the euro, 14%.

Graphic: King dollar reigns supreme

BAD NEWS

Weaker currencies, which can fuel imported inflation, are bad news for policymakers trying to contain price pressures.

The Fed accelerated the global rate-hiking cycle with some aggressive hiking from May onwards, luring more cash into the United States.

But other central banks including the European Central Bank are catching up with more aggressive hikes even as an energy crisis risks tipping economies into recession.

The ECB delivered its first 75 bps hike earlier this month. The Swiss National Bank on Thursday lifted its key rate out of negative territory and Sweden's Riksbank on Tuesday surprised with a massive 1% jump.

"I would never say never, but the ECB is not in the business of intervening in forex markets," said Marchel Alexandrovich, European economist at Saltmarsh Economics, predicting either more verbal intervention or aggressive rate hikes.

"The chorus since the summer is that if we have to hike then we are not anywhere near being done on rates."

Richard Benson, co-chief investment officer at Millennium Global Investments, said aside from the SNB, which intervenes regularly, another central bank intervention was unlikely.

He said yen weakness stood out, calculating the currency was about 50% undervalued on a purchasing power parity basis.

Analysts added that the BOJ's move, which sent the dollar down 2% on Thursday, is unlikely to work, pointing to a history of interventions which deplete foreign exchange reserves and, if not backed up by policy shifts, rarely make a difference.

Mark Dowding, chief investment officer of BlueBay Asset Management, said his fund had closed its long yen position, making a modest gain. He sees the yen as undervalued but is not ready to buy until monetary policy changes.

Neuberger's Lancioni said this week's intervention would make something of a difference - turning the dollar/yen into a "two-way trade" by squeezing some of the momentum and speculative trades that made valuations look extreme.

Graphic: Japan intervenes to prop up battered yen

(Reporting by Tommy Reggiori Wilkes, Nell Mackenzie and Dhara Ranasinghe; Graphics by Marc Jones; Editing by Dhara Ranasinghe and Josie Kao)

By Tommy Wilkes and Nell Mackenzie