ADRs (American Depository Receipts) are Chinese shares that can be traded in the United States. This allows investors in developed countries to access the growth of Chinese companies while benefiting from the visibility of US markets. Unfortunately, this sweet dream (and investors' hopes for high returns) crumbled when the central government in Beijing took control of its tech giants.

In recent years, rising geo-political tensions between the world's two largest economies have created turmoil for US-listed Chinese stocks. But what's new since late 2020 is the pressure the Chinese government itself has put on its own companies, especially technology companies. The ruling Chinese Communist Party (CCP) obsession with control and data protection led to this situation, along with the emergence of criticism from Jack Ma, founder of Alibaba, about the restrictions on the financial world in China. The CCP's reaction was swift. The fintech Ant Group was not allowed to go public and Jack Ma disappeared for a few weeks.

Subsequently, Alibaba and Tencent, the two digital giants, were fined heavily for anti-competitive practices and industry players had to polish their security policies to comply with CCP's expectations. Tencent has suspended the registration of new users in mainland China so that its software can undergo "security updates". The app previously had censorship loopholes that allowed users to share human rights-related content. More recently, Chinese authorities announced that they were banning for-profit education companies such as New Oriental Education & Training (NEET) from using the app. Education companies such as New Oriental Education & Technology and TAL Education Group are also not allowed to make a profit, go public or raise capital from foreign investors.

China's State Administration for Market Regulation (SAMR) just announced the launch of an investigation into distributors of electronic components in the automotive industry, citing suspicions of price gouging. The regulator suspects that these companies were driving up prices in the midst of a global chip shortage and has vowed to punish any stockpiling, price gouging or cartels. The CSI All Shares Semiconductor & Semiconductor Equipment Index lost 6.65% on the day. Meanwhile, in Hong Kong, tech giant Tencent Holdings lost 6.11%, after falling as much as 10.8% earlier in the session, as a Chinese media outlet called online video games "opium for the mind".

Investors should therefore be aware of the significant risks of investing in emerging Asian equities, especially in China (which is still considered an emerging country), whether directly in Hong Kong, via ETFs or via ADRs; the fall may not be over.

The Chinese pressure is certainly not over yet. And the economic war between the world's two biggest powers is still in its infancy. There are many issues that could further darken the picture: China's desire to reclaim Taiwan, the fading differences between the two political systems of China and Hong Kong,

While no one can predict what will happen next, it is certain that going up against the CCP seems similar to betting against the FED (never a good idea). Investors buying the dip could find themselves with bad news one morning, such as the breakup of their favorite companies. The threat could also come from the US, which, seeing its trade deficit with China, could announce restrictions to limit Chinese companies' access to US territory or force them to sell their products.

These disruptions are likely to last for several more months or even years. However, China, the world's second largest power, is poised to overtake the United States by 2030 (a very short time in terms of nations). Putting aside an entire part of the world economy could be negligible in the long run for an investor.

.

.

..

10 first positions

Amundi MSCI Emerging Asia ETF (AASI)

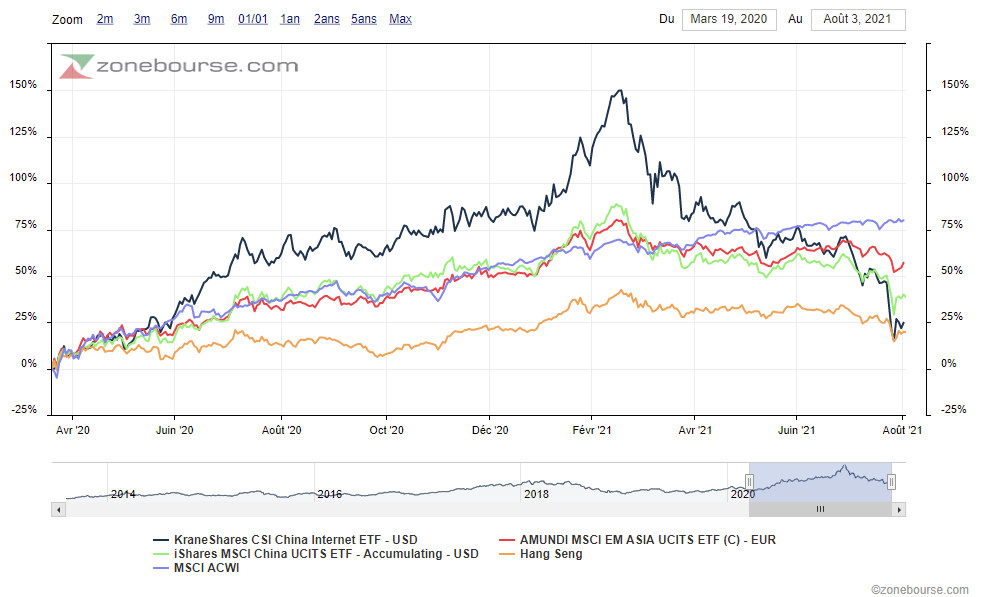

This ETF has the benefit of being more diversified by investing in all of emerging Asia (China, India, Indonesia, Malaysia) and developed Asia (Taiwan, South Korea). China accounts for almost 47.6% of the index, followed by Taiwan at 17.5%, South Korea at 16.6% and India at 12.5%. Earnings are allocated on a capitalization basis (dividends are directly reinvested). The replication is synthetic. The assets under management are substantial ('2,647 million).

.

KraneShares CSI China Internet ETF (KWEB)

This ETF focuses specifically on Chinese technology stocks, more specifically those in the e-commerce and Internet sector. It is the riskiest of the three. The underlying index fell sharply during the various Beijing government announcements (down nearly 50% since mid-February). It is essentially composed of ADR securities listed in the United States and physically held by the issuer. The assets under management are very large ($5,302 million). Fees are higher because it is a sector ETF, at 0.73%.

Comparative chart of the three ETFs and the MSCI ACWI and Hang Seng indices: