I.

With governments looking to boost the growth of domestic equity markets, the

Over the border, the recently incepted Shanghai STAR market and the Shenzhen ChiNext board (both Nasdaq look-alikes) are off to a flying start, with a raft of recently completed or reportedly planned high-profile listings, including Chinese commercial giant Ant Financial and carmaker

In this alert, we analyze important recent developments in the increasingly innovative and successful equity markets in

II.

As the world's securities exchanges look to attract the best and most valuable emerging tech unicorns, biotech firms and similarly innovative businesses, Chinese companies are at the forefront of global shifts in equity capital.

Many tech and new economy businesses come with dual-class

Since early 2018, the HKEx and the key bourses in mainland

HKEx Welcomes Emerging and Innovative Companies

Key revisions and additions to the HKEx Listing Rules (the "HKEx Rules") over the last two years—including partly moving away from the previously inviolate one-share-one-vote principle—have provided a clear path to market for businesses at the leading edge of current investment and market trends: pre-revenue biotech companies and innovative tech firms.

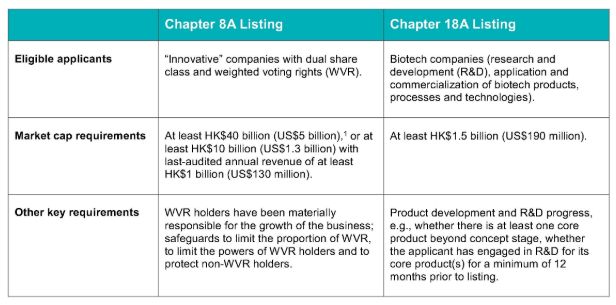

In this regard, the three new chapters of the Listing Rules—Chapter 8A (Weighted Voting Rights), Chapter 18A (Biotech Companies) and Chapter 19C (Secondary Listings of Qualifying Issuers), together with guidance letters GL92-18, GL93-18 and GL94-18—represent a significant effort by the HKEx to claim a leading role in the emerging and innovative sectors of the economic landscape.

Key Listing Suitability Criteria Under Chapters 8A and 18A of the HKEx Rules

In April of this year, the HKEx issued new guidance designed to help biotech companies highlight the value of their businesses in several key respects: R&D progress updates, disclosure of the market context and the value of in-licensed assets, as well as permitting more flexibility in the use of proceeds by listing applicants in the medical devices sector.2 From a funding point of view, the flexibility of being able to have an existing 10 percent or more shareholder in a biotech company subscribe at initial public offering (IPO) as a cornerstone investor is potentially very significant—this is not permitted for non-biotech companies, per guidance letter GL85-16.

The HKEx has clearly signaled its intention to further extend its competitive edge—it is looking to expand the WVR regime to permit (in addition to individuals) corporates to benefit from WVR3 and it has indicated that there will be additional corporate governance and Environmental, Social and Governance (ESG) requirements at the point of IPO so that listing applicants embed these key investor-facing considerations into their corporate DNA at an early stage.

Other market initiatives such as the Hang Seng TECH Index (launched on

The Shanghai STAR Market and the Shenzhen ChiNext Board

A new Nasdaq-style board for technology companies was launched by the

Over 140 companies have listed on the SSE STAR Market, with a combined market value of over

The SSE has continued to evolve the STAR Market rules so as to make it simpler for so-called "red-chip enterprises" (i.e., Chinese businesses held by overseas-incorporated listed companies quoted outside of

Following slightly behind the SSE, its keen rival, the

While the SSE has the first-mover advantage with its STAR Market rule changes from last year, the fact that the SZSE ChiNext board is a longer-established tech bourse is expected to play to its advantage as these rival exchanges vie for the top spot among

III.

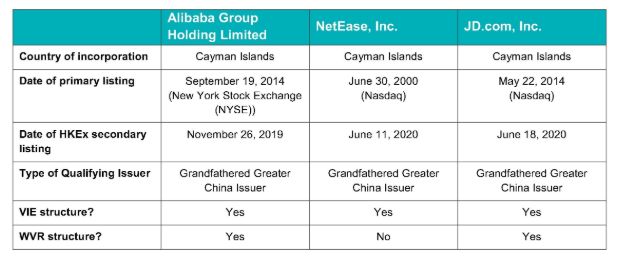

Given current geopolitical and other considerations, "large innovative companies" such as commercial behemoths Alibaba,

The concessionary secondary listing route under Chapter 19C of the HKEx Rules provides reduced listing requirements for certain Chinese companies listed on qualifying overseas exchanges, with additional concessions for "Grandfathered Greater China Issuers,8" such as exemptions from strict compliance with existing HKEx requirements on variable interest entity (VIE) and/or WVR structures.

We have also seen a steady flow of Chinese companies being privatized and de-listed from

With the recent changes to the SSE STAR Market and SZSE ChiNext listing regulations highlighted above, Chinese tech companies need no longer worry about being delayed by the CSRC waiting list as and when they choose to return home.

Footnotes

1 All USD amounts provided in this article are approximate and for reference only.

2 GL107-20 and the updated version of GL92-18.

3 Consultation Paper on Corporate WVR Beneficiaries published by the HKEx in

4 Statistics provided by the SSE as of

5 The Notice on Matters Concerning Red-chip Companies Applying for Issuance and Listing on SSE STAR Market (the "SSE Notice").

6 Rule 2.1.3 of the SSE Star Market Listing Rules (the "SSE Rules").

7 Under the SSE Notice, a pre-IPO investor must (i) undertake not to exercise any preferential rights during the IPO process, (ii) convert all its investments into ordinary shares and (iii) not have any post-listing preferential rights.

8 A qualifying issuer with its center of gravity in

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

Mr

CA 90067-6022

Tel: 202.887.4000

E-mail: Jlarivee@akingump.com; pazimi@akingump.com

URL: www.akingump.com

© Mondaq Ltd, 2020 - Tel. +44 (0)20 8544 8300 - http://www.mondaq.com, source