(via TheNewswire)

| |||||||||

Highlights:

New PEA Demonstrates the Potential for a 16-Year Mine Producing Both a Conventional 26% Copper Concentrate and a 13% Nickel Concentrate, with Associated Platinum and Palladium By-Products

The Project Presents a Pre-tax NPVof

US$463M and Post-tax NPVofUS$257M with a Post-tax IRR of 22.3% Together with an Initial Capital Cost ofUS$338M

Aggregate Indicated Mineral Resources of 19.4 Mt of Nickel, Copper, Platinum, Palladium, Gold and Copper represents a 29% Increase over the 2023 Mineral Resource Statement

New PEA Includes only the Grata, Main and Extension Deposits and the Sipilou Sud Laterite Deposit, which together with the Proposed Mine Infrastructure Covers Approximately 3% of the 835 kmProject Area

Known Mineralized Zones at Yepleu and Draba Provide Upside Expansion Opportunities, Together with the More than 10 Identified Sectors for Further Exploration Across the Project

Ivanhoe Electric Completes Earn-In and Acquires 60% of the Project

The PEA is a preliminary technical study that examines the potential for a conventional open-pit mining operation producing both a conventional copper and nickel concentrate, together with cobalt, platinum, palladium and gold as by-products. As well the Sipilou Sud laterite deposit would produce direct shipping material.

Dr.

Mr.

Highlights of the 2024 Preliminary Economic Assessment

The 2024 PEA outlines the potential for a conventional open pit mining operation supporting 86.5 million tonnes of modelled mill feed together with 1.62 million tonnes of direct shipped laterite material entirely from the Grata, Main and Extension deposits and the Sipilou Sud Laterite deposit.

Average annual production of approximately 38,627 tonnes (”) of 26% copper concentrate and 55,119 t of 13% nickel concentrate

Average annual nickel metal in concentrate of approximately 7,165 tonnes per year and copper metal in concentrate of approximately 10,043 tonnes per year

16 year-life of mine

Pre-tax Net Present Value (NPV”) at 8% discount rate of

US$463M and internal rate of return (“IRR”) of 28.2%Post-tax NPVof

US$257M and post-tax IRR of 22.3%Initial capital costs of

US$338M including a contingency ofUS$61M All-in sustaining cash costs1per pound Ni and Cu of

US$4.05 / lb before by-product credits andUS$3.00 / lb after by-product credits ofUS$1.05 / lbPost-tax payback period of 3.8 years

The 2024 PEA is preliminary in nature and includes inferred mineral resources, considered too speculative in nature to be categorized as mineral reserves. Mineral resources that are not mineral reserves have not demonstrated economic viability. Additional trenching and/or drilling will be required to convert inferred mineral resources to indicated or measured mineral resources. There is no certainty that the results of the 2024 PEA will be realized.

The 2024 PEA Demonstrates the Potential for a

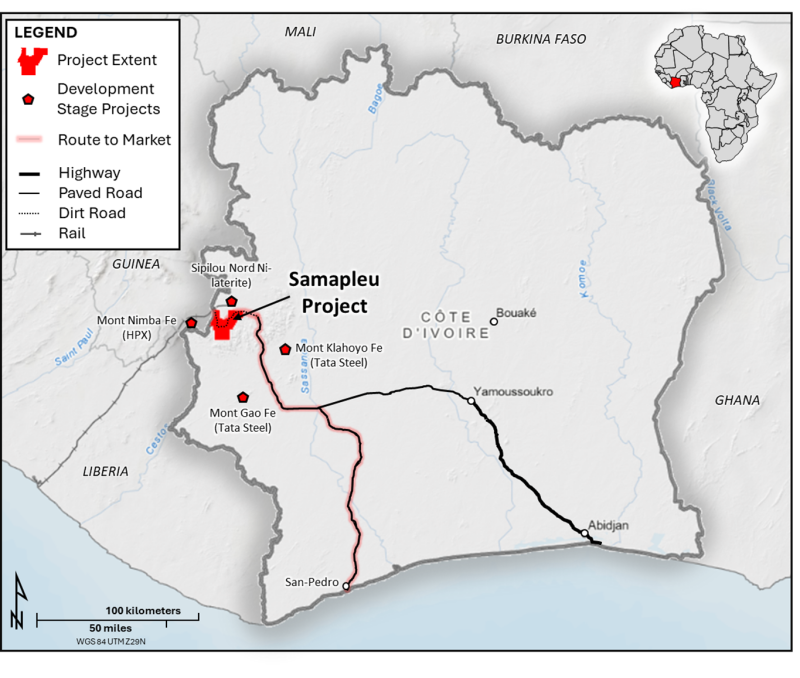

Figure 1: Samapleu-Grata Nickel-Copper Project Location in Côte d’Ivoire

Click Image To View Full Size

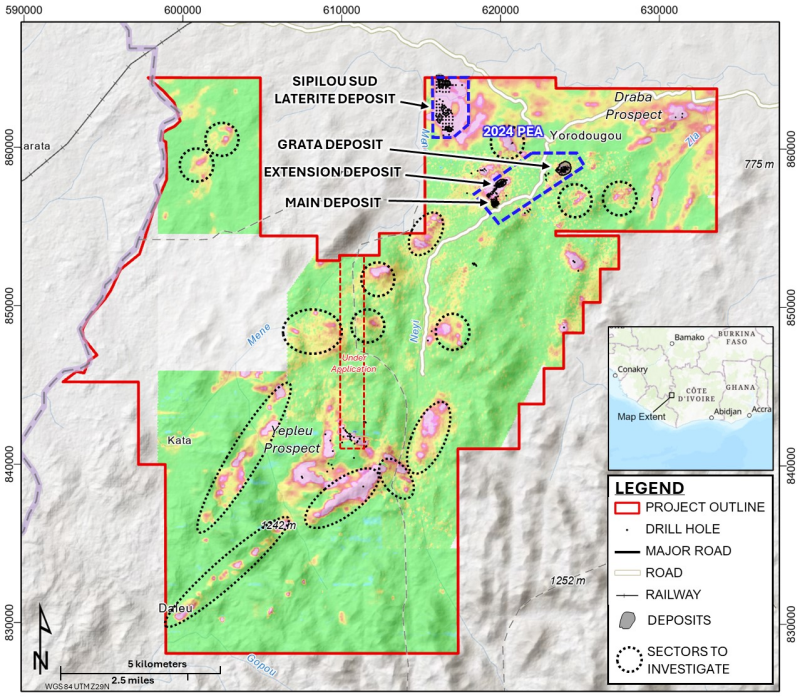

The Project consists of five exploration permits - PR838 (Samapleu-Est), PR839 (Samapleu-Ouest), PR300 (Zérégouiné), PR604 (Grata) and PR837 (Zoupleu).Figure 2 below shows the combined exploration permit areas.

Figure 2:Samapleu-Grata Nickel-Copper Project Highlighting Areas Included in the 2024 PEA and Known Prospective Sectors for Further Exploration

Click Image To View Full Size

The 2024 PEA envisages a conventional open pit mining operation with off-highway haul trucks, hydraulic excavators, and wheel loaders. The mineral resources, contained in three pits, are intended to be mined by surface operations.

The mineral processing plant is designed to process 5.475 Mtpa of run-of-mine mineralized material to annually produce 38,627 tonnes of a 26% copper concentrate and 55,119 tonnes of a 13% nickel concentrate. Both concentrates will be saleable products. No longer is it envisioned that the Project would produce either a carbonyl nickel powder or carbonyl iron powder as set out in the 2020 PEA. This eliminates the need for a refining plant with the impact most noticeable in the reduction in sustaining capital in the 2024 PEA to

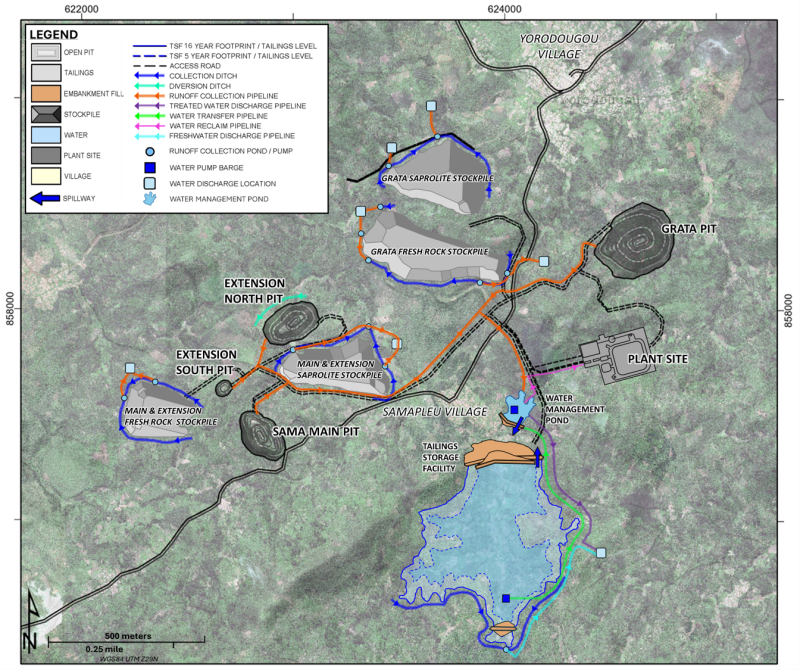

Figure 3: Proposed Layout of Project Infrastructure

Click Image To View Full Size

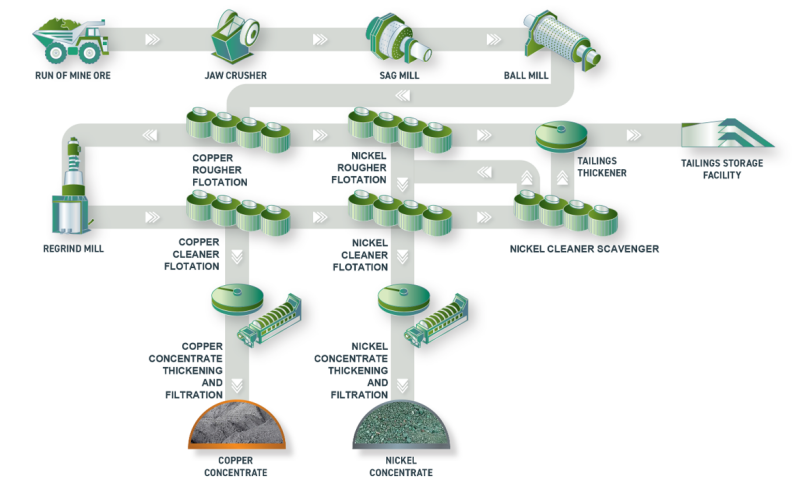

The mineral processing plant would consist of a crushing, grinding, rougher flotation, and cleaner flotation circuit. The back end of the concentrator includes tailings and concentrate thickening, concentrate filtration, and material handling.

The nickel and copper concentrates would be recovered as separate cleaned concentrates through a conventional flotation process. The tailings from the concentrator would be thickened and pumped to the Tailings Storage Facility (“TSF”). Reclaiming water from the TSF has been considered in the process design to minimize freshwater make-up to the concentrator.

Figure 4 shows the simplified version of the flow-sheet proposed for the

Figure 4: Simplified Flowsheet

Click Image To View Full Size

The TSF is designed to provide storage for the total estimated volume of tailings over the 16 year life-of-mine. The TSF would be located approximately 500 meters southwest of the plant site, adjacent to a local village and cemetery, shown on Figure 3 and constructed from saprolite and inert waste rock from open pit development. One embankment will be constructed to establish a valley type impoundment. The freshwater diversion dam will also be constructed to divert freshwater from the upstream TSF catchment area directly to the environment. The TSF location was selected based on the results of a scoping level options comparison for the Project.

Table 1 sets out the anticipated operating results for the potential future mining operations at the

Table 1: 2024 PEA Estimated Operating Results

2024 PEA Operating Results | |

Life of Mine (LOM) | 16.1 years |

Processing Rate (annual) | 5,475,000 tpa |

Processing Rate (daily) | 15,000 tpd |

Ni Concentrate | 887,414t |

Cu Concentrate | 621,888t |

Direct Ship Laterite | 1,620,000 wmt |

LOM Ni Recovery | 53.0% |

LOM Cu Recovery | 85.5% |

LOM Co Recovery | 44.8% |

LOM Pt Recovery | 54.0% |

LOM Pd Recovery | 50.3% |

LOM Au Recovery | 51.0% |

Pre-production Mined Tonnage | 5.7 Mt |

Total Mined Tonnage (including pre-production) from Open Pit Mining | 244.3 Mt |

Total Milled Tonnage from Open Pit Mining | 86.5 Mt |

Overall Mined Strip Ratio | 1.8 t:t |

Average Annual Ni Concentrate Production | 55,119 tpa |

Ni Concentrate Grade | 13% |

Average Annual Ni Metal Production | 7,165 tpa |

Average Annual Cu Concentrate Production | 36,627 tpa |

Cu Concentrate Grade | 26% |

Average Annual Cu Metal Production | 10,043 tpa |

Average LOM Mill Feed Grade | 0.25% Ni |

0.24% Cu | |

0.02% Co | |

0.10 g/t Pt | |

0.31 g/t Pd | |

0.04 g/t Au | |

Conventional Nickel and Copper Flotation underpin the Metallurgical Processes in the 2024 PEA

Over the life of mine, the Samapleu-Grata project will produce an annual average of 36,627 tonnes of a 26% copper concentrate and 55,119 tonnes of a 13% nickel concentrate through a process plant with a capacity of 5.475 Mtpa. No longer is it envisioned that the Project would produce either a carbonyl nickel powder or carbonyl iron powder as set out in the 2020 PEA.

The metallurgical testwork set out in the 2020 PEA demonstrated poor copper and nickel separation and uncertainties over the copper recovery. The 2020 PEA also assumed no revenue for precious metals nor cobalt for all of these elements would have been lost to the carbonylation residue. As a result, the 2020 PEA set out the potential for production of carbonyl nickel powder and carbonyl iron powder. The carbonyl process is relatively complex and novel, and so it was considered that constructing and operating the required refinery in a remote mine site would raise additional technical risks.

Accordingly, when work commenced for the 2024 PEA the focus turned to examining the potential to use more conventional processes that would preserve or enhance copper and nickel recoveries and allow revenue to be earned from the cobalt and precious metals. This conventional process is reasonably straightforward, carries a lower technical risk and focuses entirely on flotation, for the production of separate copper and nickel concentrates which can be sold directly to third parties without further on-site processing.

A 46-test flotation development program was undertaken on the Main and Grata Deposits which included multiple locked cycle tests. Those tests confirmed a robust flowsheet that yielded a 26% copper concentrate at up to 91% copper recovery for the Grata Deposit and 83% copper recovery for the Main Deposit along with a 13% nickel concentrate at 67% nickel recovery for the Main Deposit and 72% for the Grata Deposit. Additionally, approximately 50% to 60% of the cobalt floated in the nickel concentrate, while combined recoveries of platinum and palladium in both concentrates typically ranged from 60% to 70% with lower gold recoveries. The locked cycle nickel concentrates typically assayed between 2% and 5% magnesium oxide and fell within specification for sale to nickel smelters. Both concentrates are expected to be clean with very low levels of penalty elements such as antimony or arsenic.

Attractive Economics are Demonstrated in the 2024 PEA

The 2024 PEA outlines a potential mining operation producing 887 kt of nickel concentrate and 621 kt of copper concentrate over a 16-year mine life. The LOM all-in sustaining cash costs per pound Ni and Cu are

This produces a pre-tax NPV8of

Table 2: 2024 PEA Long-Term Metal Prices

Metal | US$/lb or /oz |

Ni | |

Cu | |

Co | |

Pt | |

Pd | |

Au |

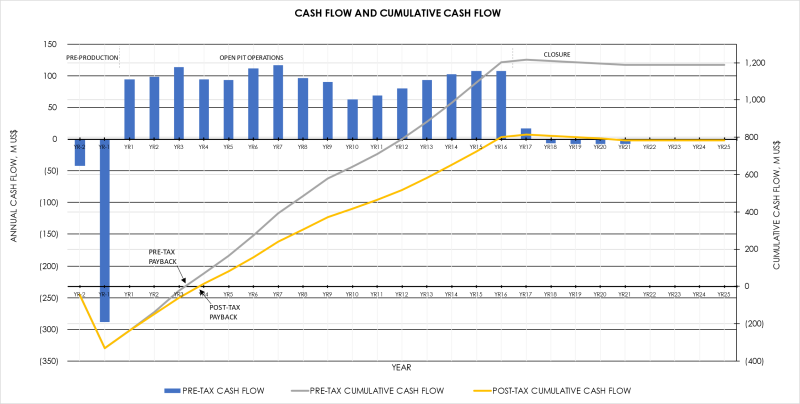

Figure 5 shows the LOM project cumulative cash flow over its 16-year mine life. The post-tax payback period is 3.8 years based on initial capital costs of

Figure 5: LOM Cash Flows

Click Image To View Full Size

The components of the initial capital cost of

Table3. 2024 PEA Initial Capital Cost Summary

2024 PEA Capital Cost Summary | US$ (millions) |

Owner’s Costs | |

Indirects | |

EPCM | |

Contingency | |

Total Initial Capital Cost |

Sustaining capital is anticipated to be

The Project also demonstrates the potential for compelling operating costs with an all-in sustaining cash cost2per pound Ni and Cu of

Table 4. 2024 PEA Operating Costs Summary

LOM Operating Costs | US$ / lb Ni & Cu |

Open Pit Mining | |

Processing | |

Tailings | |

General & Administrative | |

Royalties | |

Refining, Treatment, and Freight Costs | |

Sustaining and Closure | |

AISC per lb Ni & Cu payable | |

AISC per lb Ni & Cu payable (net of by-product credits) |

The 2024 PEA is preliminary in nature and includes inferred mineral resources, considered too speculative in nature to be categorized as mineral reserves. Mineral resources that are not mineral reserves have not demonstrated economic viability. Additional trenching and/or drilling will be requiredto convert inferred mineral resources to indicated or measured mineral resources. There is no certainty that the results of the 2024 PEA will be realized.

The

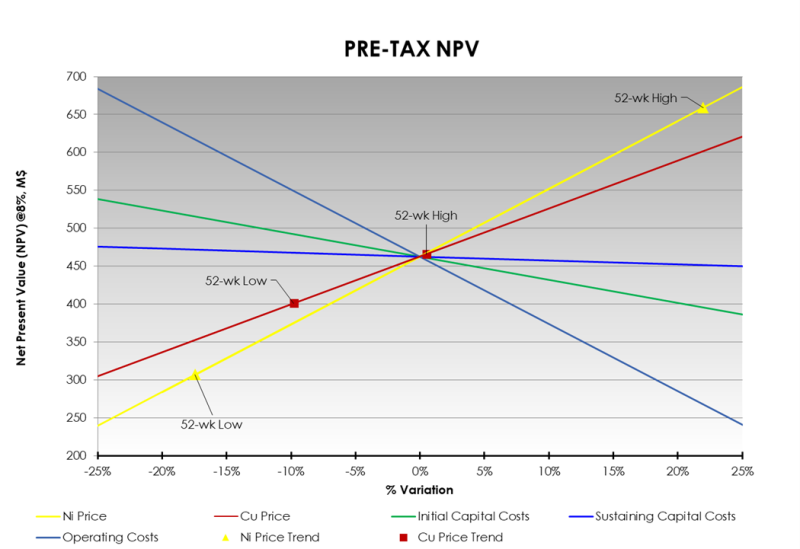

Figure 6 shows the project sensitivity to metal prices, operating cost and sustaining capital. A variation of +-10 % in metals prices modifies the NPV by +-17% while a +-10% variation in operating costs varies the NPV by +- 7%.

It is also shown that a variation of +-10% in sustaining capital costs will have an impact of +- 19% on the NPV.

Figure 6: Project sensitivity to metal pricing, operating costs and sustaining capitals.

Click Image To View Full Size

Ample Expansion Opportunities Remain to Identify Additional Mineralization within the Project’s 835 km2Footprint

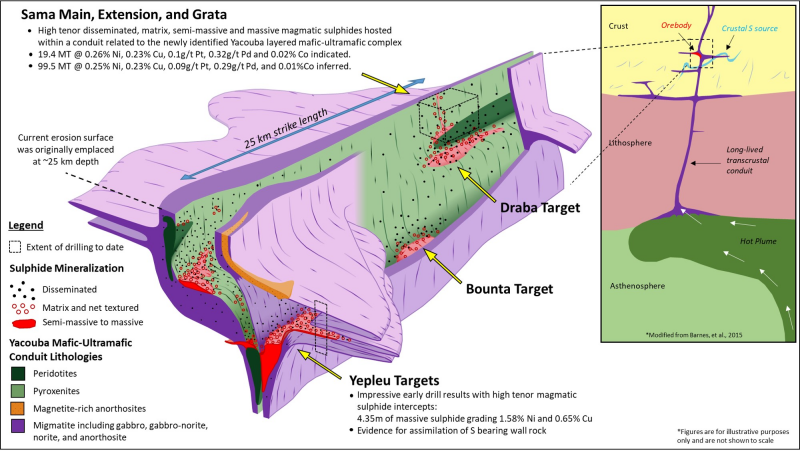

It is from this setting that the Yacouba complex has yielded the Grata, Main and Extension Deposits that form the 2024 PEA. Exploration outside of these deposits by Sama has yielded numerous targets and areas of interest, including the Yepleu, Bounta and Draba targets.

Figure 7 shows a conceptual diagram illustrating the interpreted geometry of the Yacouba complex along with the structural controls of mineralization seen in the different deposits and exploration areas of interest.

Figure 7. Conceptual Diagram illustrating the Yacouba mafic-ultramafic intrusive complex and associated magmatic Nickel-Copper-Cobalt-Platinum-Palladium mineralization.

Click Image To View Full Size

Sama geologists recognized the prospectivity of the area in the early 2010s and commenced surface mapping and sampling in areas of limited exposure along more than 30 kilometers of strike length. These efforts resulted in the identification of the

Magmatic sulfide mineralization at the

In

Similarly, the Yepleu Target was also drill tested starting in 2018 and has demonstrated similar encouraging results in both shallow and deep drilling. In

Drill hole S-341 intersecting a 21m thick mineralized magmatic pyroxenite including 2.75 m of massive sulphide at 1.02% Ni and 0.56% Cu from 13m below surface;

Drill hole S-342 intersecting a 38m thick mineralised magmatic pyroxenite with 4.35m of massive sulphide grading 1.58% Ni and 0.65% Cu from 17 m below surface; and

Drill hole S-349 intersecting 53m of combined mineralization layers grading 0.29% Ni including 2.60m at 1.31% Ni and 0.95% Cu.

Recently, Sama has started drill testing a geophysical target in the north-east corner of the property, an area called Draba.

Exploration to date has demonstrated a strong correlation between the conductive anomalies identified in airborne and ground-based electromagnetic surveys, which are highlighted in Figure 2, and the demonstrated mineralization defined within the 2024 PEA. The presence of multiple similarly conductive untested anomalies reflects the considerable exploration potential that remains within the 835 km2project area. Less than half of the conductive targets in Figure 2 have been accessed for mapping, let alone sampling or drill testing.

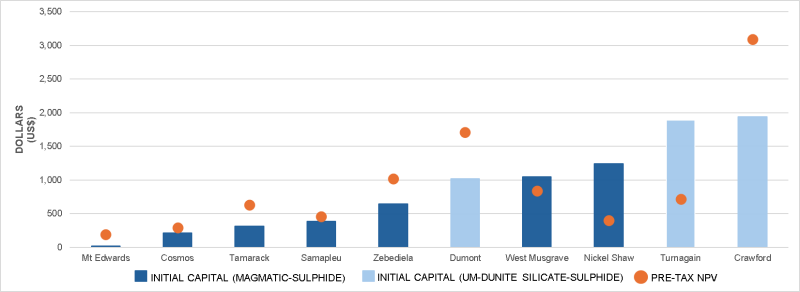

The Samapleu-Grata Nickel-Copper Project Compares Favourably to other Pre-Production Nickel Projects

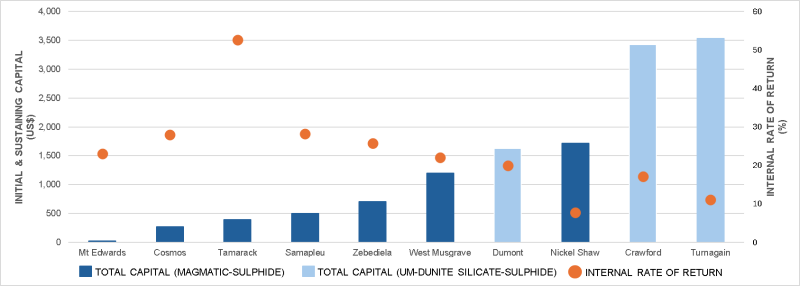

Figure 8 compares the Project’s total capital and pre-tax IRR against pre-production nickel assets, including primary magmatic sulfide deposits like Samapleu and Tamarack, as well as the bulk-tonnage low-sulfur, ultramafic-hosted deposits like Dumont and Crawford.

Figure 8. Total Capital and Pre-Tax IRR for Selected Pre-Production Nickel Deposits

Click Image To View Full Size

Source:

Figure 9 compares total capital against pre-tax NPV. The Project has a near 1:1

Figure 9.

Click Image To View Full Size

Source:

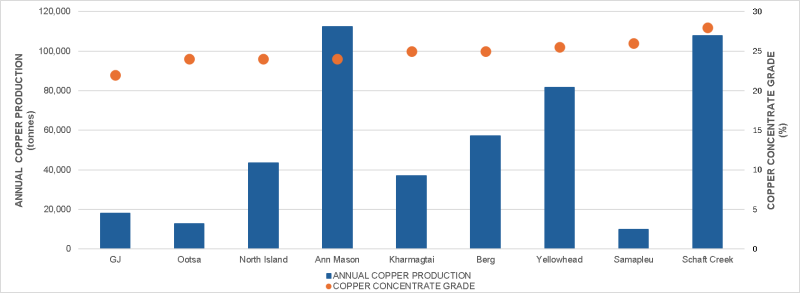

Finally, the polymetallic nature of the

Figure 10 compares the copper concentrate grade of a number of pre-production primary copper assets with copper head grades < 0.3% and which would produce copper concentrate which shows that, even though production would initially be small, the Project’s copper concentrate quality compares favourably to that which would be produced from primary copper mines.

Figure 10. Copper Concentrate Production and Grade of Certain Pre-Production Copper Deposits Producing Copper Concentrate

Click Image To View Full Size

Source:

2024 PEA Based on Updated

The 2024 PEA is based on an updated Mineral Resource Estimate (Table 6 and Table 7), which has an effective date of

Table 6. Mineral Resource Estimate for the Main, Extension and Grata Deposits at the

Classification | NSR Cut-off | Deposit | Tonnes | Ni (%) | Cu (%) | Pt (g/t) | Pd (g/t) | Au (g/t) | Co (%) |

Indicated | Main | 15,248,000 | 0.26 | 0.22 | 0.10 | 0.31 | 0.04 | 0.02 | |

Extension | 514,000 | 0.25 | 0.16 | 0.10 | 0.45 | 0.02 | 0.02 | ||

Grata | 3,645,000 | 0.28 | 0.29 | 0.11 | 0.32 | 0.04 | 0.02 | ||

Total | 19,407,000 | 0.26 | 0.23 | 0.10 | 0.32 | 0.04 | 0.02 | ||

Inferred | Main | 21,342,000 | 0.25 | 0.21 | 0.07 | 0.28 | 0.04 | 0.02 | |

Extension | 10,885,000 | 0.28 | 0.22 | 0.10 | 0.48 | 0.02 | 0.02 | ||

Grata | 67,272,000 | 0.24 | 0.25 | 0.10 | 0.26 | 0.04 | 0.01 | ||

Total | 99,499,000 | 0.25 | 0.23 | 0.09 | 0.29 | 0.04 | 0.01 |

Mineral Resource Statement Notes:

1.CIM definition standards were followed for the resource estimate.

2.The 2024 resource models used ordinary kriging (OK) grade estimation within a three-dimensional block model with mineralized domains defined by wireframed solids.

3.Mineral resources are constrained within pit shells.

4.Open pit NSR cut-off of

5.The NSR used for reporting is based on the following:

a.Long term metal prices of

US$8.83 /lb Ni,US$3.99 /lb Cu,US$1,146 /oz Pt,US$1,218 /oz Pd,US$1,700 /oz Au,US$22.62 /lb Cob.Metallurgical recoveries are based on grade recovery curves for the various elements in a copper concentrate and nickel concentrate.

c.Bulk density was determined by a regression formula based on iron (Fe) for each lithology with each deposit.

d.Mining cost of

US$4.08 /t mined includes saprolite removal, incremental mining by bench and sustaining capital.

6.Saprolite material were assigned zero grade due to the lack of metallurgical test work.

7.Mineral Resources that are not mineral reserves do not have economic viability. Numbers may not add due to rounding.

8.The resource estimate was prepared by

9.Modeling was performed using Datamine Studio RM software, with grades estimated using ordinary kriging (OK) interpolation methodology. Samples were composited at 3.0 m down hole. Assessment of the raw samples indicated a variety of capping levels for each element by domain and deposit. Block grades were estimated on a multi pass basis with a minimum and maximum number of composites and maximum number of composites per drillhole required for each estimation pass. Block size is 10 m (x) by 10 m (y) by 10 m (z) with up to three sub-blocking divisions comprising a minimum block size of 1.25 m (x, y, and z).

The change in the updated mineral resource model for the Main, Extension and Grata Deposits compared to the 2023 mineral resource model is due to locating missing downhole surveys which have now been included. This resulted in a 127%, 51% and 11% increase in the number of surveyed holes at the Grata, Extension and Main Deposits respectively which has allowed for a reclassification of the resource. That reclassification has resulted in an increase in indicated mineral resources to 19.4 Mt, a 29% increase over the 2023 Mineral Resource Statement.

A maiden mineral resource estimate was also completed for the Sipilou Sud Laterite Deposit which is physically separate from the sulphide deposits.

Table 7. Maiden Mineral Resource Estimate for the Sipilou Sud Laterite Deposit at the

Classification | Ni % Grade Cut-off | Deposit | Tonnes | Ni (%) | Co (%) |

Inferred | 1.10 | Sipilou South | 2,095,000 | 1.75 | 0.05 |

Mineral Resource Statement Notes:

1.CIM definition standards were followed for the resource estimate.

2.The 2024 resource models used ordinary kriging (OK) grade estimation within a three-dimensional block model with mineralized domains defined by wireframed solids.

3.Mineral resources are constrained within pit shells.

4.Open pit Ni cut-off of 1.10% is based on the cost/tonne for direct shipping of the laterite.

5. The cut-off grade considered used for reporting is based on the following:

Long term metal prices of

US$8.83 /lb Ni andUS$22.62 /lb Co.Bulk density was determined by evaluating 1,002 samples collected from diamond drillholes.

Complete direct ship cost of

US$38.40 /wmt mined.Mining cost of

US$4.08 /t mined includes saprolite removal, incremental mining by bench and sustaining capital.

6.Saprolite material were assigned zero grade due to the lack of metallurgical test work.

7.Mineral Resources that are not mineral reserves do not have economic viability. Numbers may not add due to rounding.

8.The resource estimate was prepared by

9.Modeling was performed using Datamine Studio RM software, with grades estimated using ordinary kriging (OK) interpolation methodology. Samples were composited at 1.0 m down hole. Assessment of the raw samples indicated a variety of capping levels for each element by domain and deposit. Block grades were estimated on a multi pass basis with a minimum and maximum number of composites and maximum number of composites per drillhole required for each estimation pass. Block size is 40 m (x) by 40 m (y) by 2 m (z) with up to three sub-blocking divisions comprising a minimum block size of 10 x 10 x 0.5 meters (x, y, and z).

NATIONAL INSTRUMENT 43-101 DISCLOSURES

A technical report (the “Technical Report”) with respect to the

For readers to fully understand the information in this news release, they should read the Technical Report in its entirety when it is filed on SEDAR, including all qualifications, assumptions, and exclusions that relate to the information to be set out in the Technical Report. The Technical Report is intended to be read as a whole, and sections should not be read or relied upon out of context.

The following companies have undertaken work in preparing the 2024 PEA:

BBA International Inc. Knight Piésold Ltd.

The independent Qualified Persons responsible for preparing the 2024 PEA are:

Todd McCracken ,P. Geo . –BBA International Inc. Bahareh Asi ,P. Eng . –BBA International Inc. Kevan Ford ,M. Eng . –BBA International Inc. Jason Van Schie ,P. Eng . –BBA International Inc. Chris Martin ,C. Eng . – Independent ConsultantWilson Muir ,P. Eng . – Knight Piésold Ltd.

Each Qualified Person has reviewed and approved the information in this news release relevant to the portion of the 2024 PEA for which they are responsible. By virtue of education and relevant experience, the aforementioned are independent Qualified Persons for the purpose of NI 43-101.

Any other scientific and technical information contained in this news release not related to the 2024 PEA has been reviewed, verified, and approved by Dr.

About

Sama is a Canadian-based, growth-oriented resource company focused on exploring the Samapleu nickel-copper project in Côte d’Ivoire,

For more information, please visit www.samaresources.com.

About Ivanhoe Electric Inc.

Ivanhoe Electric is a

FOR FURTHER INFORMATION, PLEASE CONTACT:

Dr.

Tel: (514) 726-4158

Mr.

Tel: (604) 443-3835 or (877) 792-6688, Ext. 5

Tel: (416)-644-2020 or (212)-812-7680

www.renmarkfinancial.com

Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

Certain of the statements made and information contained herein are "forward-looking statements" or “forward-looking information” within the meaning of Canadian securities legislation. Forward-looking statements and forward-looking information such as “will”, could”, “expect”, “estimate”, “evidence”, “potential”, “appears”, “seems”, “suggest”, are subject to a variety of risks and uncertainties which could cause actual events or results to differ from those reflected in the forward-looking statements or forward-looking information, including, without limitation, the ability of the company to convert resources in reserves, its ability to see through the next phase of development on the project, its ability to produce a pre-feasibility study or a feasibility study regarding the project, its ability to execute on its development plans in terms of metallurgy or exploration, the availability of financing for activities, risks and uncertainties relating to the interpretation of drill results and the estimation of mineral resources and reserves, the geology, grade and continuity of mineral deposits, the possibility that future exploration, development or mining results will not be consistent with the Company's expectations, metal price fluctuations, environmental and regulatory requirements, availability of permits, escalating costs of remediation and mitigation, risk of title loss, the effects of accidents, equipment breakdowns, labour disputes or other unanticipated difficulties with or interruptions in exploration or development, the potential for delays in exploration or development activities, the inherent uncertainty of cost estimates and the potential for unexpected costs and expenses, commodity price fluctuations, currency fluctuations, expectations and beliefs of management and other risks and uncertainties.

Forward-looking statements and forward-looking information are based on various assumptions. Should one or more of these risks and uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in forward-looking information or forward-looking statements. Accordingly, readers are advised not to place undue reliance on forward-looking statements or forward-looking information.

In addition, all of the results of the 2024 PEA constitute forward-looking statements or information and include future estimates of internal rates of return, net present value, future production, estimates of cash cost, proposed mining plans and methods, mine life estimates, cash flow forecasts, metal recoveries, and estimates of capital and operating costs.

Except as required under applicable securities legislation, the Company undertakes no obligation to publicly update or revise forward-looking statements or forward-looking information, whether as a result of new information, future events or otherwise.

The PEA completed for the Company is preliminary in nature and includes inferred mineral resources, considered too speculative in nature to be categorized as mineral reserves. Mineral resources that are not mineral reserves have not demonstrated economic viability. Additional trenching and/or drilling will be required to convert inferred mineral resources to indicated or measured mineral resources. There isno certainty that the resources development, production, and economic forecasts on which this PEA is based will be realized.

1 AISC includes all operating costs, treatment and refining charges, sustaining capital and closure costs.

2 AISC includes all operating costs, treatment and refining charges, sustaining capital and closure costs.

Copyright (c) 2024 TheNewswire - All rights reserved.

Copyright (c) 2024 TheNewswire - All rights reserved., source