INTRODUCTION

If a person thinks one thing but says another, what are others to believe? Statutory interpretation often favors the latter over the former. But within the context of controlled foreign corporations ("

The dispute concerns the 2017 tax year, when Altria owned slightly more than 10% of ABI, measured by both vote and value. The balance was held by non-

Altria filed its 2017 tax return in accordance with the rule change, but it then sued for a refund.2 The basis of its claim is that the 2017 rule change went against the plain reading of the statute as well as

STOCK ATTRIBUTION UNDER C.F.C. RULES

In a purely domestic context,

Until the T.C.J.A. was enacted in 2017, the policy of Subpart F was to prevent certain intercompany transactions undertaken by a

Attribution Rules

The 10% and more-than-50% thresholds are measured not just by direct ownership of foreign corporate shares, but also through indirect ownership arising by application of the attribution rules of Code §318. This provision generally attributes stock ownership to persons related to the actual shareholder.

The attribution rules fall under three categories.

-

First, an individual shareholder's stock may be attributed to certain family members.

- Second, stock owned by an entity, such as a corporation, may be attributed to the entity's owners. This category of attribution is known as upward attribution.3

- Third, stock in other corporations actually owned by an owner of an entity may be attributed to that entity. This is known as downward attribution. If the entity is a corporation, downward attribution only applies if the shareholder holds at least 50% of the corporation. But if this threshold is met, all stock held by the shareholder is attributed to the corporation, rather than downward attribution to the to the shareholder's ownership percentage in the corporation. For example, if a shareholder holds 50% of a corporation, then the corporation is deemed to hold all other stock held by the shareholder rather than 50% of the stock in another corporation.

In some, but not all, instances, these rules can apply multiple times. If a person is deemed to own stock via attribution, the stock can be attributed again to another person. Suppose a shareholder of a corporation is deemed to own the stock of the corporation's subsidiary. The subsidiary stock can be further attributed to the shareholder's family members.

The

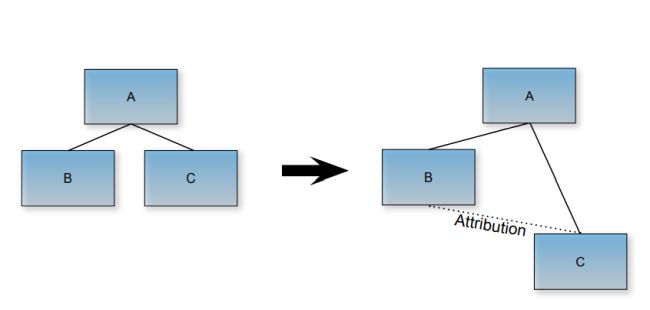

The following diagram shows a standard application of downward attribution. B, being a corporation owned by A, is deemed to own other stock held by A (namely, stock in C).4

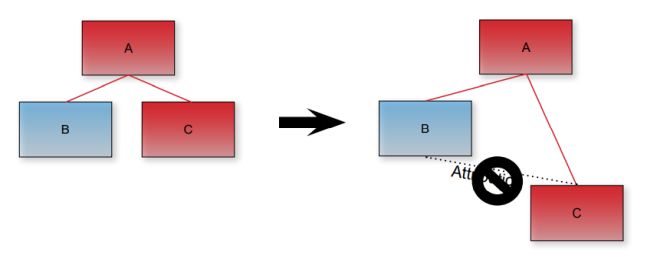

Now suppose A is a foreign corporation. Prior to the effective date of the T.C.J.A., Code §958(b)(4) barred downward attribution from a foreign person to a

This is no longer the case with the repeal of that provision.

APPLICATION TO ALTRIA

The following diagram shows, in relevant part, the structure of Altria vis-ŕ-vis ABI.

Altria directly held 10.2% of ABI. Through the application of the indirect ownership rules and constructive ownership, Altria was also deemed to hold 10.2% of each of the foreign ABI subsidiaries. ABI directly or indirectly wholly owned each subsidiary, and Altria was considered to hold its proportionate 10.2% share of ABI's 100% ownership. The result was that while Altria was a

The analysis became more complicated with the T.C.J.A. With downward attribution now freely applicable, ABI US was deemed to own the stock held by its parent, ABI. Therefore, ABI US actually and constructively held all of the shares of ABI Subs 1, 2, and 3. With the latter two subsidiaries, ABI US's ownership was entirely constructive, as it did not directly hold shares in either subsidiary.

Because a

Altria's Arguments

Altria's claim for a refund rests on two main arguments. First, it believes that treating Subs 2 and 3 as

The legislative history adds that the 10% threshold for counting

Plainly, neither Altria nor ABI US effectively control ABI or Subs 2 and 3. Consistent with this argument, Altria's complaint emphasizes that it has little influence on ABI's governance.

Second, Altria cites legislative history relating to the repeal of Code §958(b)(4) to point out that situations like Altria's were not meant to be captured by the repeal. The repeal was aimed at situations where a foreign-owned

Outside that fact pattern, it seems

This provision is not intended to cause a foreign corporation to be treated as a controlled foreign corporation with respect to a

In fact, the

The conference report language for the bill does not change or modify the intended scope [of the above statement].

In other words, the complete repeal of Code §958(b)(4) may have been a result of a misunderstanding. Altria's evidence makes clear that at some point, the

With both arguments, Altria believes an understanding of congressional intent is required to apply the rules as intended by

CONCLUSION

Many commentators agree with Altria's characterization of the repeal as "absurd."12 But whether Altria's desired method for undoing the absurdity will succeed is uncertain. For the moment, Altria has petitioned the court to stay proceedings until Moore, another prominent lawsuit regarding

Footnotes

1. The business is perhaps better known as Philip Morris, its originator, predecessor, and affiliate.

2.

3. If the entity is a foreign entity, a slightly different set of rules apply under Code §958(a)(2).

4. Note that in parallel, C is deemed to own stock of B.

5. Note that while ABI US's constructive ownership caused Subs 2 and 3 to become

6. President's 1961 Tax Recommendations: Hearings Before the H. Comm, on Ways & Means, 87th Cong., 1st Sess.

7.

8. H.R. Rep. No. 115-409, at 387 (2017); H.R. Rep. No. 115-466, at 507-508 (2017).

9.

10. 163 Cong. Rec. S8, 110 (2017).

11.

12. Citing

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

NY 10155

Tel: 212755.3333

Fax: 212755.5898

E-mail: bueno@ruchelaw.com

URL: www.ruchelaw.com

© Mondaq Ltd, 2024 - Tel. +44 (0)20 8544 8300 - http://www.mondaq.com, source