|

|

| This week's gainers and losers |

| Up: Avis +57.51%: the car rental company, along with peer Hertz (+10%), is entering its third straight week of gains amid airport chaos. The stock is trading at its highest level since April 2022. Nebius +33.22%: boosted by the world’s largest market cap company, the technology infrastructure specialist is currently negotiating the acquisition of Israeli startup AI21 Labs, which specializes in artificial intelligence. AOI +44.93%: a $71 million order for transceivers from a "hyperscaler" delighted shareholders of the fiber-optic products supplier. This unnamed customer is no stranger to the company: since mid-March, it has placed a total of $124 million in orders. Intel +23.82%: partner with Google? Intel did not hesitate for long. The two companies will work together across several generations of Intel Xeon processors with the goal of improving Google’s infrastructure as a whole. UMG +13.56%: Bill Ackman is putting $55.75 billion on the table to acquire the music major. Pershing Square’s offer of EUR 30.40 per share represents a 78% premium, forcing key shareholders Bolloré and Vivendi to weigh in on the group's future. Western Digital Corporation +16.43%: a wave of buy ratings is hitting the hard drive specialist. Bernstein raised its price target from $170 to $340, Evercore ISI from $310 to $370, and Morgan Stanley from $369 to $380. Paramount +11.55%: a sprawling deal, to be sure, but one that is nearing the finish line. The entertainment group has secured financing from 18 banks for the acquisition of Warner Bros. Discovery. The transaction is expected to close in the third quarter, subject to regulatory approvals. Down: Texas Pacific -7.71%: the sudden death of a board member has unsettled investors. Murray Stahl was the CEO of Horizon Kinetics Holding Corporation, the company’s largest shareholder. |

|

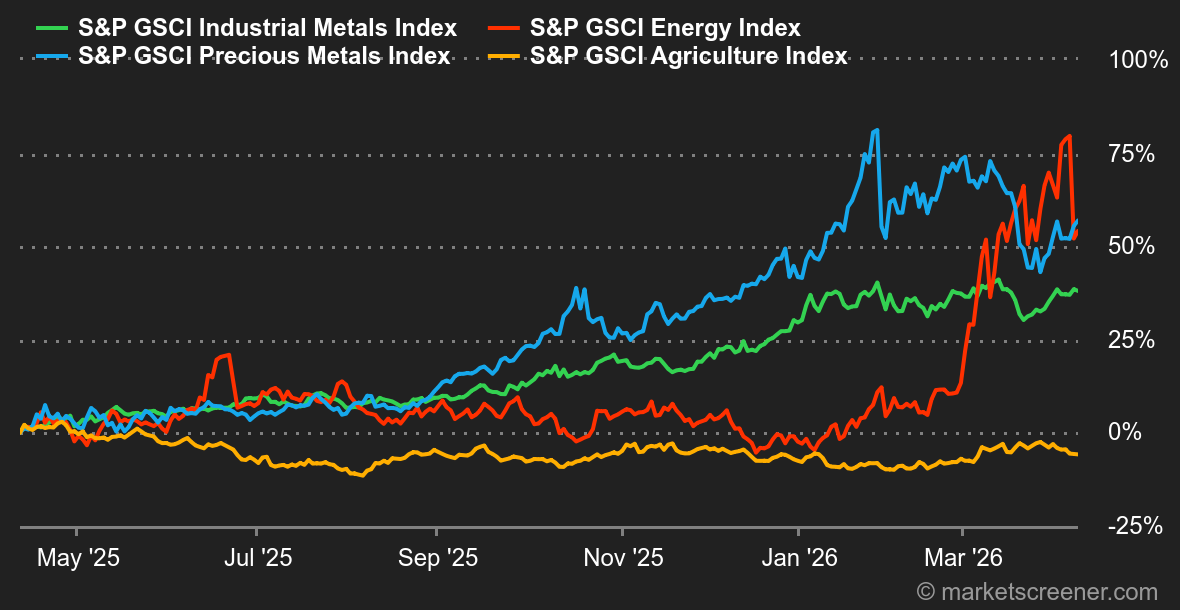

| Commodities |

Energy: Oil prices ended the week down sharply, by roughly 11%. Brent crude is trading around $95.50 per barrel (June 2026 contract) and WTI around $97.60 (May 2026 contract). The weekly drop was driven by the announcement of a two-week ceasefire between the United States and Iran, which temporarily calmed the market. However, prices rebounded on Friday. Traders remain concerned about renewed supply threats in the Middle East and the ongoing closure of the Strait of Hormuz. The truce agreement between Washington and Tehran remains fragile, and fighting continues in the region. Today, maritime traffic through the Strait of Hormuz accounts for only a small fraction of its usual volume. Iran is demanding transit fees from commercial vessels crossing the area. The United States is firmly rejecting that condition. Investors are therefore waiting for the outcome of the next round of diplomatic talks, scheduled for this weekend, to assess the chances of a lasting agreement. Metals: Gold is regaining favor with investors and has posted a second straight week of gains, reaching $4,800. The announcement of a temporary two-week truce between the United States and Iran initially explains the move, since it cooled oil prices and, by extension, eased inflation fears. However, prices remain highly unstable. Reports of ceasefire violations and continued clashes are limiting gold’s upside. On the industrial metals side, copper is advancing in London to $12,700, its highest level in three months. Agricultural products: Wheat posted its steepest weekly decline since late July. The drop came directly after the release of the U.S. Department of Agriculture’s monthly report. The agency reported global inventories well above expectations. As a result, wheat is trading lower at 571 cents per bushel (May 2026 contract). Corn is following the same downward trend at 443 cents, while soybeans are holding up better with a slight gain (1,166 cents). |

|

| Macroeconomics |

Macro: The ceasefire, however fragile, reached between Iran and the United States gave investors a much-needed boost. Risk assets rebounded sharply, especially equities, while the dollar naturally lost ground. Bonds and oil, meanwhile, have been more hesitant: after a steep selloff immediately following the announcement, both markets recovered as investors waited for concrete action, starting with the reopening of the Strait of Hormuz. As a result, the German 10-year yield is holding above its breakout level of 2.90%, supported not only by energy-related inflation fears but also by stronger financing needs to support investment spending. Until the improvement is confirmed, a measure of caution still makes sense in allocation decisions. Crypto: In line with equity indexes, bitcoin (BTC) rebounded 4.55% this week and is now trading around $72,000. The same trend can be seen in spot Bitcoin ETFs, which have recorded $455 million in net inflows since Monday. Other major cryptocurrencies are following the leader: ether (ETH) is up 5% and has moved back above $2,200, Solana (SOL) is gaining 2% at around $83, while XRP is up 1.3% at $1.34. This week, the crypto angle in the geopolitical backdrop is directly tied to the Strait of Hormuz. According to the Financial Times, Iran reportedly said that every oil tanker using the shipping corridor will have to declare its cargo by email and pay a fee equivalent to $1 per barrel, payable in bitcoin, several other cryptocurrencies, or Chinese yuan. The goal would primarily be to avoid the U.S. dollar and the potential sanctions associated with it, although this remains highly tentative at this stage and still needs to be confirmed. |

|

|

| Things to read this week | ||||||

|

|

*The weekly movements of indexes and stocks displayed on the dashboard are related to the period ranging from the open on Monday to the sending time of this newsletter on Friday. The weekly movements of commodities, precious metals and currencies displayed on the dashboard are related to a 7-day rolling period from Friday to Friday, until the sending time of this newsletter. These assets continue to quote on weekends. |